The Value Evaluation Model of Forestry Investment Projects Based on Real Options

-

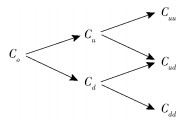

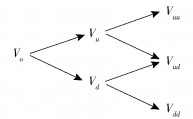

摘要: 林业投资项目具有典型的收益不确定性、投资不可逆性、自然增值性和管理灵活性等特点, 需要选择合理适用的决策方法。传统的林业投资项目评估大多采用净现值法, 忽视了林业投资项目的期权特性, 容易引起决策的偏差和错误的判断。从实物期权的视角, 分析了林业投资项目的实物期权特性, 包括扩张、缩小、放弃期权以及递延期权。基于二叉树理论构建了林业投资项目的实物期权价值评价模型, 并且运用实例进行了验证, 对林业项目投资的不同阶段分别进行研究。实例证明, 基于实物期权模型的林业投资项目决策更有科学性。Abstract: Uncertainty of return, investment irreversibility, natural appreciation and management flexibility are typical characteristics of forestry investment projects; therefore, a reasonable and applicable decision-making method is necessary in a forestry investment project. The net present value (NPV) is widely applied in traditional evaluation of investment projects, but this method ignores options, which easily leads to inaccurate decision and wrong judgement. In this paper, we analyze the real options in forestry investment projects, including expanding options, narrowing options, abandoning options and deferring options. Then we build a real option value evaluation model based on binomial tree options pricing model, and verify the model in a real project, in which there exist different options in different stages. It is proven that the real option evaluation model is much more feasible and more accurate in forestry investment projects.

-

-

[1] 魏均, 梅斌, 张绍文.基于实物期权的林业项目评估[J].商业研究, 2006(6):44-47. doi: 10.3969/j.issn.1001-148X.2006.06.012 [2] 徐雪漫, 宋维明.评价林业投资的实物期权方法[J].林业经济问题, 2004, 24(2):115-117. doi: 10.3969/j.issn.1005-9709.2004.02.015 [3] 贺晓波, 王冬梅, 曾诗鸿.附碳汇收益的林业投资项目价值评估——基于实物期权定价理论[J].中国管理科学, 2017, 25(3):20-29. http://www.wanfangdata.com.cn/details/detail.do?_type=perio&id=90717175504849554851484851 [4] KALLIO M, OINONEN S. Real options valuation of forest plantation investments in Brazil[J]. European Journal of Operational Research, 2012, 217(2):428-438. http://www.wanfangdata.com.cn/details/detail.do?_type=perio&id=242cf30d35d52076628653105b770e82

[5] REGAN C M, BRYAN B A, CONNOR J D, et al. Real options analysis for land use management: methods, application, and implications for policy[J]. Journal of Environmental Management, 2015, 161:144-152. http://smartsearch.nstl.gov.cn/paper_detail.html?id=15a8ab8e5f7fd9703481296e8dc6a8b9

[6] 《中国林业发展道路》课题组.中国林业发展道路的研究课题报告摘要[J].林业经济, 1992(1):10-14. http://www.cnki.com.cn/Article/CJFDTotal-LSZG199201002.htm [7] 魏均.基于实物期权方法的林业投资项目评价问题研究[D].北京: 北京林业大学, 2006. http://cdmd.cnki.com.cn/Article/CDMD-10022-2006162816.htm [8] 梁贺红, 卢远新.沉没成本效应研究述评[J].经营管理者, 2009(3):22-23. http://www.cnki.com.cn/404.htm [9] 姚梅.不确定环境下的实物期权定价[D].重庆: 重庆大学, 2009. http://cdmd.cnki.com.cn/article/cdmd-10611-2009149600.htm [10] HAN T J S, LENOS T.战略投资学: 实物期权和博弈论[M].狄瑞鹏, 译.北京: 高等教育出版社, 2006. [11] 杨春鹏, 吴冲锋, 吴国富.实物期权中放弃期权与增长期权的相互影响研究[J].系统工程理论与实践, 2005, 25 (1): 27-31. doi: 10.3321/j.issn:1000-6788.2005.01.004 [12] 曾勇, 邓光军, 夏晖, 等.不确定条件下的技术创新投资决策:实物期权模型及应用[M].北京:科学出版社, 2007. [13] 黄杉琴.基于实物期权理论的林业项目投资决策研究[D].北京: 北京林业大学, 2013. http://cdmd.cnki.com.cn/Article/CDMD-10022-1013213947.htm [14] JAMIE R.战略、价值与风险: 不动产期权理论[M].宋清秋, 译.北京: 经济管理出版社, 2003. [15] 田野.多阶段投资决策的复合期权模型及应用[D].哈尔滨: 哈尔滨工业大学, 2007. http://cdmd.cnki.com.cn/Article/CDMD-10213-2008194174.htm [16] 陈安琪, 崔偌晗, 张卫民.基于实物期权法的林木资产价值评估——以江西吉安东固采育林场为例[J].林业经济, 2017(11):70-75. http://www.wanfangdata.com.cn/details/detail.do?_type=perio&id=673839007

下载:

下载:

图(2)

/

表(14)

计量

- 文章访问数: 1283

- HTML全文浏览量: 474

- PDF下载量: 35